Services

Actuarial Valuations

The accounting of retirement benefits has become a major concern for many global multinational corporations operating in Japan. We can help their subsidiaries report the actuarial valuation results to their head office on time with excellent “quality”, “speed” and “price”.

Quality

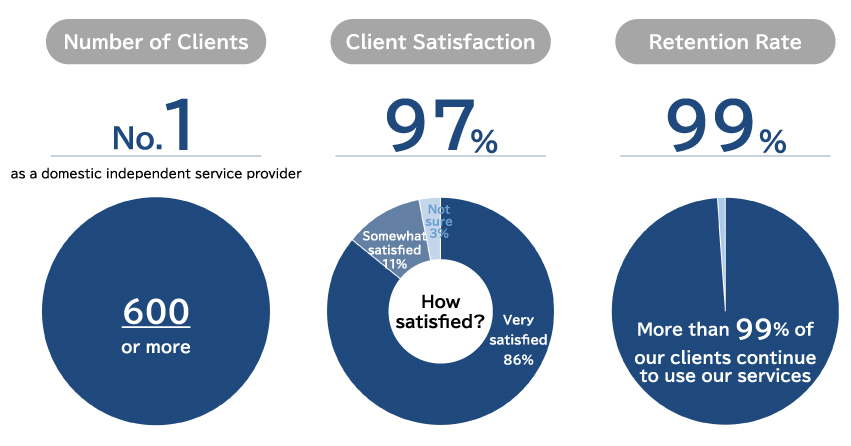

We are the leading independent firm providing actuarial valuation services to more than 700 clients.

Furthermore, to meet the latest regulatory requirements by the respective standards, our pension actuaries monitor any related legislation and announcements by accounting boards. This enables us to support our clients in meeting their financial reporting obligations with confidence.

Speed

We can provide calculation results within one month of receiving member data and scheme information. This can be coordinated to meet tight reporting deadlines (including on the first business day after the reporting date).

In addition, using our tools, we can follow up quickly with changes in assumptions as required.

Price

Our standard valuation service is available for the following fee (excluding consumption tax):

IFRS (IAS) or US GAAP valuations: From JPY 700,000

For multiple plans, we charge JPY 250,000 for each additional plan.

This service includes actuarial reports written in English.

Additionally, the calculation of 10-year expected benefits is included in U.S. GAAP valuation.

(Japanese GAAP valuations can be provided if necessary)

Our Actuarial Valuation Services are highly valued by our clients

※2022 Client Survey(conducted between July 1st, 2022 and June 30, 2023)

Plan Design and Harmonization

Your Challenges

For employers, the purpose of providing a retirement plan varies in terms of HR and financial perspectives. Retirement plans are expected to improve attraction and retention, motivation of employees, and encourage post-retirement savings. They may involve, however, various challenges including financial from a potential market downturn, administration costs, and lack of recognition by the employees.

In addition, there are some features specific to the Japanese pension market as follows.

- A DB (Defined Benefit) plan to DC (Defined Contribution) plan conversion in a typical developed western market would commonly include a reduction in the value of benefits by reducing its future service even for existing employees. However, the norm in Japan is often that there is little or no reduction in benefits for past and future service.

- In Japan, there are relatively low limits for making contributions to a DC plan. Given this, employers may not be able to completely provide the desired benefit level through a DC plan alone.

- Employee consent is legally required in order to newly implement a DC plan (by union or employee representative) or convert DB past accrual to DC (by 2/3 of employees).

Our Solutions

With our wealth of experience and consulting know-how, we provide clients with innovative, value-added solutions.

- Knowledge and experience in comprehensive review, redesign and harmonization of retirement plans for many Japanese companies and foreign affiliates

- Successful results in retirement benefit consulting, including DB to hybrid plans and DC plan conversions

- Tailored consulting services to meet the unique needs and situations of each client

- Truly unbiased and independent consulting advice. We do not provide any brokering, plan administration, asset management or trustee services. Therefore, we can give advice without conflicts of interest.

Our Consulting Approach

Plan design project is broken into several phases as follows:

Current plan analysis and objective setting

- Analyze the current plan (employee demographics, level of pensionable salary etc.)

- Set objective from HR and financial perspectives

Plan design

- Examine new plan design alternatives and develop relevant pros and cons on the available funding structure

- Set new plan parameters and check accrual patterns of current and new plan using an employee model

- Check the impact on the individual employees (consider make-up arrangement if necessary)

- Analyze long-term cost impact

Implementation

- Provider selection

- DC investment option selection

- Employee communication

Implementation Assistance

Our implementation services include the following key areas of support.

Employee communication

A new pension plan design/redesign is not successful unless employees appreciate the features of the new plan. Furthermore, employers lawfully must obtain employee consent. We believe that employee communication is critical part of a successful project.

Provider selection

There are so many plan administrators registered with the Ministry of Health, Labor, and Welfare and it must be a difficult task for employers to select the best administrator. In addition, DC regulation requires that employers with more than 100 employees choose a DC plan administrator through comparison of the services and fees of three candidates or more.

DC investment option selection

Investment returns for DC participants in Japan have historically been very low. This is mainly due to the concentration of DC assets in low-risk investments (which in the past have had returns that hover around zero). To aim for better returns, a proper line-up of investment options should be provided. This could be particularly important in times of inflation.

Assistance for government application

We can assist employers in preparing the drafts of amended work rules and related regulations reflecting new plan introductions or plan changes that are required when applying to the government.