Key Considerations for Managing Defined Benefit Pensions in a Rising Interest Rate Environment:

Rethinking Assets and Liabilities from a Holistic Perspective

Published: 7 July 2026

Translation of our original Japanese article dated 1 May 2026

Contents

- Current Interest Rate Trends and Their Impact on Asset Management

- The Nature of Rising Interest Rates in Defined Benefit (DB) Plans

- Are Rising Interest Rates a Tailwind or a Headwind?

- How Should Asset Allocation Be Redesigned?

- DB Plan Management Based on Your Plan’s Specific Design

- Conclusion

1. Current Interest Rate Trends and Their Impact on Asset Management

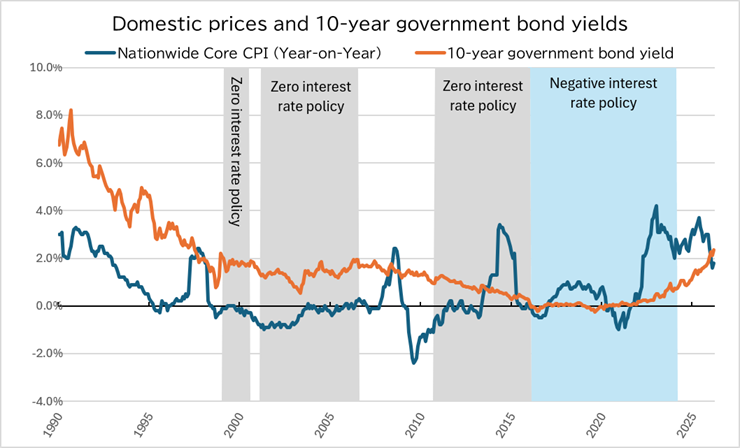

Recently, there has been a noticeable rise in domestic interest rates. The yield on 10-year Japanese government bonds climbed to 2.49%, the highest level since 1997. This increase appears to reflect stronger concerns about the future path of domestic interest rates. Upward pressure on rates had already been building as monetary policy shifted away from its previous easing stance and began allowing interest rates to rise from suppressed levels. In addition, concerns about inflation, driven by supply uncertainties in petroleum-related products, have further heightened market caution.

(Data source: Bloomberg)

(Data source: Bloomberg)When interest rates rise, it is often thought that bond prices will fall. In practice, for corporate pension plans that hold domestic bonds, this can translate into short-term losses. In addition, during periods when inflation accelerates and monetary policy is tightened rapidly, both equities and bonds can fall at the same time, reducing the benefits of portfolio diversification. The U.S. market in 2022 is a typical example of this, with both U.S. dollar-denominated equities and bonds posting a loss of around 18 percent1.

1 In 2022, the return on the MSCI World Index (Net, USD) was negative 18.1 percent, while the return on the FTSE World Government Bond Index (USD) was negative 18.3 percent. (Data source: MSCI, FTSE)

2. The Nature of Rising Interest Rates in Defined Benefit (DB) Plans

Liabilities Also Change at the Same Time

However, when considering corporate pension plans, it is important to note that it’s not sufficient to only look at the assets. In defined benefit pension plans, a rise in market interest rates generally leads to a reduction in liabilities.

For example, in a typical pension plan, if the discount rate used for retirement benefit accounting increases, the present value of retirement benefit obligations are reduced. Similarly, if the assumed rate of return used for pension funding purposes increases, actuarial liabilities also reduce.

The assumed rate of return for pension funding is set by the sponsoring employer based on a reasonable long-term outlook for investment returns. If expected returns on pension assets improve in line with rising market interest rates, there may be greater scope to raise this assumption.

In other words, even if rising interest rates result in temporary losses on pension assets, the overall impact on the pension’s financial position may be limited or could even improve when assets and liabilities are considered together.

This is a key difference between general asset management and the management of corporate pension plans.

3. Are Rising Interest Rates a Tailwind or a Headwind?

Given what was discussed in the previous section, it is not appropriate to view rising interest rates as a headwind across the board. A healthy increase in interest rates driven by economic expansion in Japan would likely act as a tailwind for DB plan management, not only by reducing pension liabilities but also through improvements in equity market conditions.

On the other hand, in a scenario where cost-push inflation accelerates and monetary policy is tightened rapidly, there is a risk that economic activity may weaken excessively, eventually leading to declines in both equity prices and interest rates. In such a case, pension assets would suffer, while liabilities would also tend to increase, resulting in a more significant negative net impact on the plan.

Unfortunately, the current global environment is highly uncertain, making it difficult to form a clear view on which path the current rise in interest rates will take.

When managing corporate pension plans, it is therefore increasingly important not to respond to rising interest rates simply by reducing the allocation to domestic bonds out of concern. Instead, a more integrated approach is required, one that manages assets and liabilities together.

4. How Should Asset Allocation Be Redesigned?

The Role of Domestic Bonds in a Higher Interest Rate Environment

Thinking about the increasing yield environment, it is worth re-examining the role of domestic bonds. During the era of ultra-low interest rates, they were often viewed as assets with limited return potential, while carrying significant downside risk in the event of rising interest rates.

However, now that interest rate levels have begun to recover, domestic bonds have regained their appeal as income-generating assets. In addition, during periods of economic slowdown, they can help support the portfolio through price appreciation.

Domestic bonds should therefore not be seen simply as low-return assets. Rather, they deserve to be re-evaluated as core holdings that align well with pension liabilities.

At the same time, it is important to reassess the role of hedged foreign bonds and alternative investments that were introduced as substitutes for domestic bonds during the low interest rate era. These assets were incorporated to supplement returns and improve portfolio diversification. However, although less visible, they also carry risks such as liquidity constraints and valuation lags. Given the change in the environment, it is no longer sufficient to assume that these assets will remain necessary simply because they have worked in the past. It is important to carefully re-examine whether they can continue to fulfill the same role. This should be done from the perspective of both their sources of return and their risk characteristics.

5. DB Plan Management Based on Your Plan’s Specific Design

Of course, the arguments made in this blog do not apply uniformly to all pension plans. In cash balance or similar type plans, rising interest rates do not necessarily lead to a reduction in liabilities. In addition, revisions to the discount rate used in retirement benefit accounting may be subject to time lags and materiality thresholds unique to Japanese GAAP.

Therefore, it is not sufficient to rely on general statements such as “rising interest rates are beneficial for DB plans”. Instead, you need to assess the implications based on your own plan design, accounting treatment, and benefit structure.

6. Conclusion

Pension Management in a Higher Interest Rate Environment

In an inflationary environment, even if nominal benefit levels are maintained, their real value declines. At a time when securing talent and investing in human capital are becoming increasingly important, corporate pension plans are no longer seen merely as employee benefits, but as a key component of employee compensation. Viewed in this way, the additional financial flexibility created by rising interest rates can serve not only to strengthen the stability of the plan, but also as an opportunity to review benefit levels and enhance the overall attractiveness of it.

What matters in managing corporate pension plans during a period of rising interest rates is not to focus solely on gains and losses from asset management. Instead, you need to review the plan as a whole, including liabilities, benefit design, and accounting treatment, and gradually move away from the mindset shaped by a low interest rate world. Looking ahead, pension management will require more than just defensive responses. It will be important to consider how to build a new balance that is appropriate for a higher interest rate environment. This shift in thinking may well have a significant impact on the quality of pension plan management going forward.

*Please note that the views expressed in this column are those of the author.

About the Author

Akihito Takagi

Chartered Member of the Securities Analysts Association of Japan (CMA)

Graduated from the Department of Economics and Business Law, Faculty of Economics, Yokohama National University.

Worked at a government-affiliated financial institution, where responsibilities included asset management as well as securities and settlement operations. Also held secondments to an affiliated investment advisory firm, the Japan Mutual Aid Association of Public School Teachers, and the Organization for Small & Medium Enterprises and Regional Innovation, engaging in the management of pension and mutual aid funds. Joined IIC Partners Co., Ltd. as a consultant in June 2020.